The senior housing industry is facing steep challenges that shift each day as the Covid-19 pandemic spreads and the nation’s response evolves. In this dynamic environment, making predictions could be a fool’s errand, yet owners, operators and investors are seeking some basis around which to craft strategies.

With this in mind, here are three scenarios based on analyses from equity analysts and other industry professionals, touching on key concerns related to occupancy, the length of the Covid-19 crisis, and what recovery might look like.

Still bracing for a hit on occupancy

After years of oversupply suppressed occupancy, senior living providers were just starting to experience census increases when the coronavirus outbreak escalated in the United States. In the early weeks of the pandemic in this country, occupancy appears to have held steady or even increased for some providers. About 80% of operators saw no significant increase in move-outs, and 21% experienced occupancy increases, according to an Activated Insights survey of 19 operators, representing more than 100,000 units, which was conducted over March 18 and March 19.

Bloomfield, New Jersey-based Juniper Communities is among those providers that clocked an occupancy increase, according to a March 20 letter from CEO Lynne Katzmann.

“For many older adults, living alone without a good support system, we are a great option, especially now,” Katzmann wrote in her letter. “No need to go to the pharmacy or grocery store; someone to clean and disinfect; health and medical care will come to you rather than you having to go out. Many older adults and their families understand this.”

Still, the pandemic has dramatically changed sales and marketing, with tours curtailed and new residents are subject to more rigorous health screening and even potential quarantines for a period of time after moving in. These changes raise the possibility that sales pipelines will slow, move-ins will lag, and occupancy will fall.

Finally, there is the stark and unfortunate fact that Covid-19 is especially fatal for older adults. Communities that experience coronavirus outbreaks could experience occupancy declines for the tragic reason that residents pass away. These scenarios also could depress demand for senior living.

Green Street analyst Lukas Hartwich quantified this risk by drawing on expert estimates that 33% to 100% of the U.S. population could ultimately be infected, and the mortality rate for seniors is in the 5% to 15% range. These are wide ranges, particularly in terms of the potential infection rates, and Hartwich considered various scenarios depending on different combinations of infection rate and seniors’ mortality rate. For instance, if the Covid-19 infection rate is 50%, and the mortality rate for seniors is 15%, this could result in a demand being reduced by 7.5% and occupancy decreasing 8%, according to Hartwich’s March 16 note.

There are complicating factors to consider when thinking through how Covid-19 will end up affecting senior living occupancy. One open question is whether assisted living communities will begin taking on a significant number of patients who are moved out of skilled nursing facilities, as SNFs take patients from hospitals that need to open up beds for Covid-19 patients. Already, authorities in New York state issued a directive that nursing homes must take patients from hospitals.

Pandemic duration: ‘Eventually we get it’

The question of when the Covid-19 outbreak in the United States will be brought under control or wane is among the most pressing and difficult to answer, as it depends on a broad array of variables.

Analysts with Raymond James created various duration scenarios and assigned a likelihood of each one occurring, based on factors such as the availability and development of therapeutics; comments made publicly and to Raymond James by government officials and business leaders; the testing situation; overall medical preparedness; and the fact that warmer weather appears to slow the spread of Covid-19.

The likelihood of each Raymond James scenario is likely to change, the firm’s analysts noted, based on actions taken by government leaders and the response of the public.

As of March 22, their most likely scenario was dubbed the “Procastinator” or “Eventually We Get It” situation, which they assigned a likelihood of 45%. These are some of the hallmarks of this scenario:

— Communities impacted by Covid-19 “shut down,” but first drag their feet and do not act preemptively

— The public largely ignores warnings about the need for social distancing until the death rate commands their attention, which Raymond James estimated would occur by April 1

— At that point, the entire U.S. economy essentially grinds to a halt, testing “dramatically increases,” and within two weeks, the rate of new infections slows

— Total infections remain below 1 million, and “we will have turned a corner by Memorial Day”

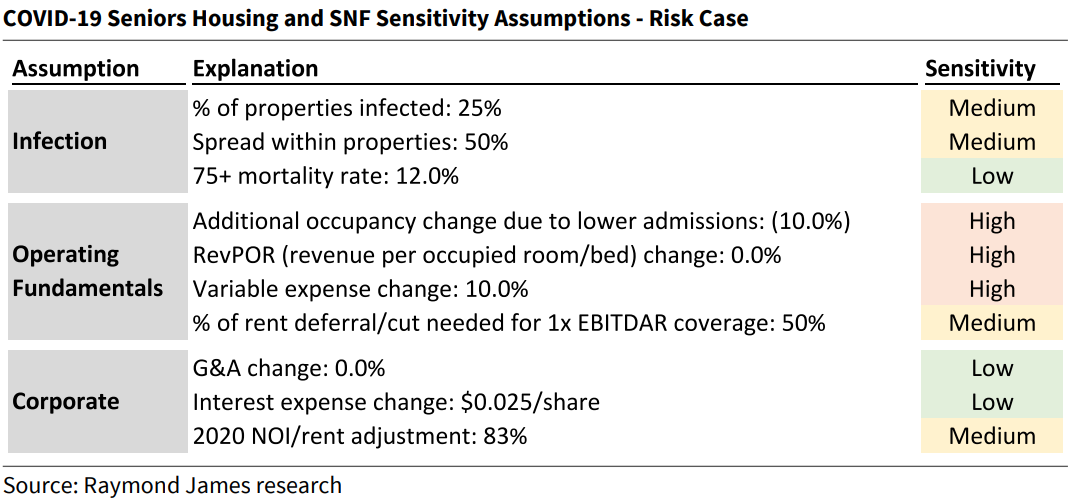

Analyst Jonathan Hughes and Research Associate Mike Bell relied on this scenario in calculating a senior housing and skilled nursing-focused sensitivity analysis, which included assumptions such as 25% infection rate for properties and a 12% mortality rate for the 75-plus population, with a 10% occupancy change due to lower admissions and variable expense change of 10%.

The second most-likely scenario envisioned by Raymond James was dubbed “Saved by Summer.” In this case, both the government response and actions taken by public fail to limit the spread of infections, and the virus doubles every week until warmer summer weather provides a respite and a chance to take more effective action, with a turning point coming by July 4. As of March 22, the Raymond James analysis put the likelihood of this scenario at 35% — an increase from the firm’s initial projections, based on statements from the White House that nationwide lockdown would not be necessary.

“Failure IS an Option” is a scenario in which “governments at all levels” fail to take meaningful action and summer does not slow down the virus spread, which would result in more than 150 million infections and an ongoing crisis as of Labor Day. The analysts pegged the likelihood of this scenario at 15%, and noted that it would become more likely in the absence of “significant government actions.”

Finally, Raymond James outlined a scenario called “Stop Everything Now,” under which the government shut down all non-essential businesses at the outset of the U.S. outbreak and ramped up testing at the same time, resulting in a late-April timeframe for “turning the corner.” But the government has likely already missed the window to hit that late-April turning point, they noted.

Optimism around industry recovery

There is no doubt that Covid-19 is putting enormous strains on the industry in the near term, but many senior housing professionals — such as Premier Senior Living Group founder Wayne Kaplan — have expressed optimism about what a recovery will look like when it does come.

Capital One Analyst Daniel Bernstein believes that there could indeed be a “sharp drop” in occupancy this year and next year, but also that there are several reasons why two-year plus outlook for the industry could be “shockingly good,” he wrote in a March 13 note.

New construction starts could “crash to zero or near zero” as a result of Covid-19, he wrote, with new supply growth likely to be less than 1% even two years out. This would be due to Covid-19 fears as well as the pandemic’s impact on capital markets. Yet, the pandemic will not change the basic demographic makeup of the country, which includes a huge wave of aging baby boomers.

If demand growth of 2% to 3% per year holds steady, occupancy could increase by 150 to 200 basis points per annum for “several years” starting in 2022 or 2023, with net operating income growing “well north” of 5% in that timeframe.

These years could be especially fruitful for REITs, if the pattern from the last economic crisis holds. If the REITs’ stock prices rebound, they could hold a cost-of-capital edge over private buyers coming out of the Covid-19 slump, and build up their portfolios as they did in the 2010-2015 time period.

Transactions could be abundant in the aftermath of Covid-19, several M&A advisors and capital providers have told SHN in the last two weeks, as the pandemic is likely to motivate mom-and-pop operators to sell.

While these prognostications paint a relatively rosy picture of the senior housing recovery, there are of course major variables that could come into play; economists are “mixed” on the possible long-term effects that Covid-19 will have on the economy, with disruption to supply chains, globalization trends and business confidence creating significant question marks, National Investment Center for Seniors Housing & Care (NIC) Chief Economist Beth Mace wrote in a March 23 newsletter.

And even if the best predictions come true and the senior housing industry rebounds from the pandemic quickly and decisively from a business perspective, providers will also have to contend with the emotional and psychological toll that the coronavirus crisis is inflicting on their staffs, residents, residents’ family members, and older adults generally.

As Mace put it, the Covid-19 pandemic will “bring unforgettable grief and sadness,” calling for ongoing “support, solutions, encouragement and assistance,” especially for those working on the frontlines.

The post 3 Covid-19 Predictions for Senior Housing: Occupancy, Pandemic Duration, Industry Recovery appeared first on Senior Housing News.

Source: For the full article please visit Senior Housing News

Be First to Comment